The pension choices that could give you a €1.5 million boost

Conor O'Shaughnessy, specialist pensions advisor with Elevate Financial Planning.

, CFP®, Elevate Financial, offers valuable advice for anyone considering their investment options

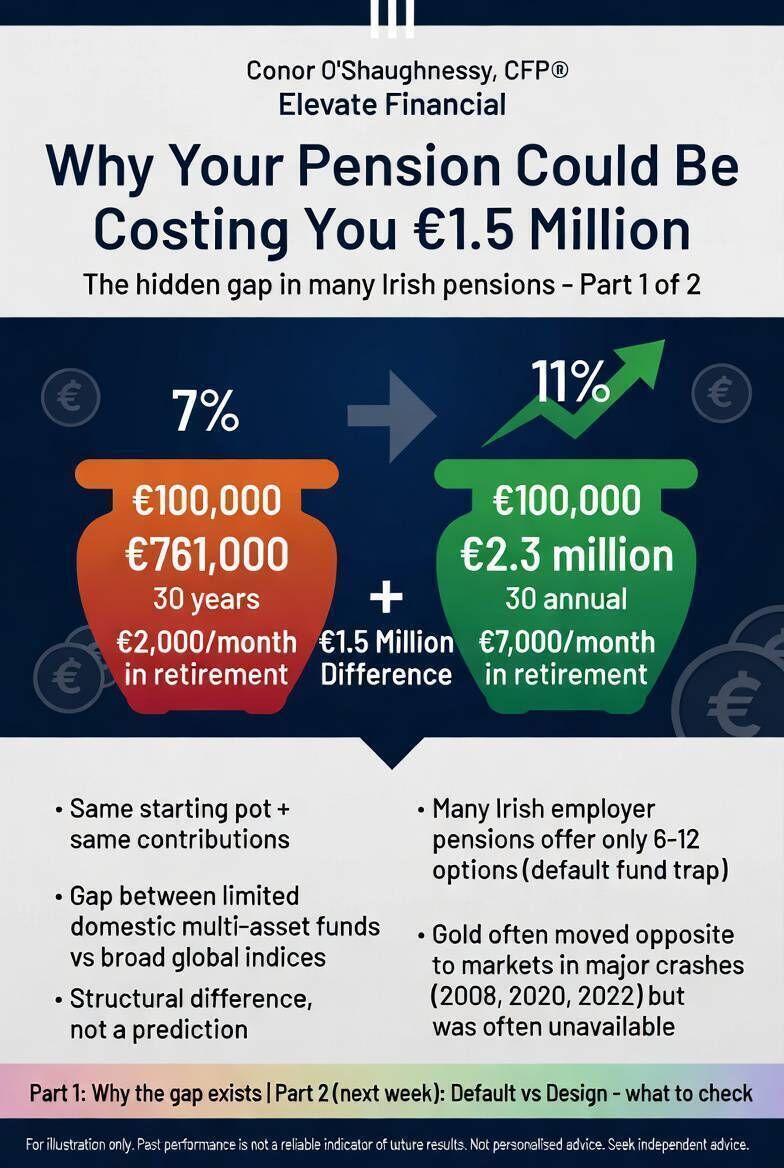

If you have a €100,000 pension today, where it is invested right now could be the difference between retiring with €761,000 or €2.3 million.

That is not a typo.

That is the difference between drawing down roughly €2,000 a month in retirement and €7,000 a month. Same starting point. Same contributions. Completely different life.

That gap comes down to one thing. The difference between a pension growing at 7% per year, which is broadly where most standard Irish employer schemes land over the long term, and one growing at 11%, which is closer to what broad global indices have delivered over the last 50 years.

After 20 years that gap is over €400,000. After 30 years it is over €1.5 million.

To do this properly I have to go into some detail. You cannot get this knowledge in a couple of sentences and I am not going to pretend otherwise. The only investment this requires from you is your concentration. Give it that, and your future self could be very grateful that you did.

I cannot guarantee you what equity markets are going to do. The past is the past and it is not a reliable guide to the future. All investments can fall in value and you may get back less than you invest. The next 50 years may look very different to the last 50.

My argument is not that equities are going to return 11% over the next 50 years. I genuinely do not know what they will return. Nobody does.

What I am arguing is something more specific. The relative gap between a well-structured globally diversified portfolio and a limited domestic multi-asset range has been remarkably consistent regardless of what markets have done in absolute terms. If global equities return 11%, domestic multi-asset funds have historically returned closer to 7%. If equities return only 5% over the coming decades, those same domestic structures, based on their consistent pattern of relative underperformance, would likely return closer to 3%.

The gap is structural. That is the argument. Not a promise of 11%.

What I can say, with confidence grounded in decades of data, is that you can structure your pension so the probability of a meaningfully better outcome is in your favour. That is what this article is about.

I also want to acknowledge something. The 7% figure I use for standard domestic ranges over the long term may itself be generous. I do not want to overstate the case. Consistent 50-year track record data for Irish domestic pension funds is genuinely difficult to source, as most funds do not have records stretching that far back. However, in every fund I have examined with data stretching to 20 or close to 40 years, those funds have significantly lagged the global indices over the same periods. I have not reviewed every fund available in Ireland. But across nearly two decades in this industry, every time I have examined a domestic multi-asset fund with a track record stretching to 20 years or beyond, the same pattern has emerged. Not occasionally. Every time. That consistency is what I am describing when I say the gap is structural.

The one thing I want to be transparent about, I am compensated when clients implement the solutions I recommend. I believe genuinely in what I do, but you should know my recommendation is not conflict-free. What I can tell you is this, based on everything the data shows, my wholehearted belief is that net of all fees, including ours, you will come out considerably ahead in the scenario I'm describing compared to where most people currently sit. That is not a guarantee, but that is what the evidence consistently points to.

This is primarily written for anyone with a former employer pension who assumes those 6 to 12 funds are as good as anything out there, and for anyone who simply wants to make sure they are getting the absolute best possible outcome from their pension. If that is you, read on.

If you are currently receiving financial advice, this article is still worth reading and it should get your full attention. We can have an honest and healthy debate about the approach I am advocating and the historical data behind it. That is a conversation I welcome.

If you are within five years of retirement, have a low tolerance for investment risk, or have a complex financial situation, the questions raised here are still worth considering. But the answers will depend heavily on your personal circumstances and a conversation with an advisor who understands your full picture is essential before making any changes. This article is not suitable as a basis for any investment decision without independent personalised advice.

Now some of you reading this may already be in one of the higher performing funds. Over the last 10 years, some of the higher performing multi-asset funds available in Ireland have delivered returns closer to 11%. That is genuinely good and worth acknowledging. Over that same 10 year period however, the S&P 500 and MSCI World delivered somewhere between 13 and 15% per year as of end of February 2026. Even at the top end of the Irish market the gap has still been there. And if you are in a standard default option, the gap is considerably larger.

But even those higher performing options, when you stretch the data out over 20 to 50 year periods, have typically delivered returns in the region of 8 to 9% per year. Still meaningfully behind the global indices which have delivered 10.45% to 11.71% over the same very long periods.

Now, a fair question at this point is whether comparing a multi-asset fund to a pure global equity index is a fair comparison at all. A multi-asset fund holds bonds, property, cash and alternatives alongside equities. A global index is all equities. They are not the same thing and it would not be fair to pretend otherwise.

But here is why I think the comparison is still valid in practice.

If someone wants a multi-asset approach, better-performing options have historically existed outside the domestic ranges available to most Irish pension holders. The global asset managers I have referenced offer multi-asset funds with longer track records and deeper resources than most of what is available domestically. So even on that point the domestic range loses the argument.

But my own view, backed by the data I have outlined throughout this article, is that for the growth portion of your portfolio a passive index tracker is the superior choice in the vast majority of cases. The evidence for that position has been building for decades and it is not going away.

In the years when markets have fallen hard, growth-oriented multi-asset funds domestically available in Ireland have historically fallen in very similar ways to a pure equity index. Sometimes less. Sometimes just as much. And in some cases more. So the defensive instruments within those funds have not historically provided the cushion that the fund structure implies. Meanwhile assets that have historically provided genuine non-correlation were simply not available or not used within those domestic ranges.

Consider the most significant market downturns of the last 50 years.

In 1973-1974, when the oil crisis triggered a bear market that cut equity values by nearly 50% in real terms, gold more than quadrupled. It was one of the best-performing assets of the decade.

In 1987, when global markets fell approximately 23% in a single day and over 30% in the following months, gold held its ground and finished the year positive.

During the dot-com crash between 2000 and 2002, when the Nasdaq fell nearly 80% and global equity markets dropped sharply for three consecutive years, gold delivered strong positive returns in each of those years.

In 2008, when global markets fell approximately 37%, gold rose approximately 6% in euro terms.

In 2020, when markets crashed during Covid, gold rose approximately 25% in US dollar terms. For a euro investor, that was closer to 14%, as the euro strengthened against the dollar that year.

In 2022, when markets fell significantly and even cautiously managed domestic multi-asset funds fell around 12%, gold delivered approximately 6.5% for a euro-based investor.

Five distinct crises. Six if you split 2000-2002 into individual years. Across every single one, gold moved in the opposite direction to equities at precisely the moment it was needed most. And in every single case, it was sitting entirely outside the reach of most Irish employer pension holders.

Gold will have its down periods as well. It is not risk-free. The point is not that it always rises when equities fall, but that it has historically behaved differently at key moments. When markets are strong, gold can be flat or lag. During periods of stress, inflation or uncertainty, it has often provided diversification.

The data is the data. And when you look at the years that were supposed to demonstrate the value of the multi-asset approach, the domestic ranges largely fell with the market anyway. While instruments that actually worked in those years were sitting outside the ranges most people had access to. That is not a coincidence. That is a structural problem with limited domestic access.

At some point in almost every year over the last 98 years, markets have dropped by at least 6%. Roughly one in four years has been negative. That is normal. That is the price of admission.

It is the opposite of a casino. The longer you stay in a casino, the more likely you are to lose money. With the stock market, history shows the inverse is true. The longer you stay invested, the more the odds move in your favour. It is not about timing the market. It is about time in the market.

Consider what happened in 2008, the worst year in living memory for global stock markets. If you had invested everything right at the peak before that crash, you would have watched your pension fall sharply. But by 2012, you were back to even on a total return basis. By 2018, you had more than doubled your money. By 2021, you had nearly quadrupled it.

The cost of doing nothing has often been greater than the cost of market volatility.

So the question becomes very simple. Look at 2022 as an example. Sitting in a growth multi-asset fund versus simply buying the S&P 500: is falling closer to 14%, and in some cases as high as 22%, in a bad year instead of 18.3%, while missing out on roughly 3% to 4% per year over the long term, really a good deal? I have yet to find anyone who sits with that comparison and thinks it is.

And for most people in Ireland, nobody has ever explained why that gap exists, or that it was avoidable with the right tools and the right access.

In Part 2, I will show you exactly why that gap exists, what the real-world numbers look like across a full market cycle, and the three specific questions you need to ask to find out whether your pension is built on default or design.

If any of this has raised questions about your own former employer pension, those questions are worth pursuing. The answers are usually simpler than people expect, and the difference they make rarely is.

To arrange a free introductory consultation with Conor O'Shaughnessy CFP, visit calendly.com/conor-s-qq4/introductory-financial-consultation

- This article is for educational and informational purposes only and does not constitute personalised financial advice. Past performance is not a reliable indicator of future results. All investments can fall as well as rise in value. You should seek independent financial advice tailored to your own personal circumstances before making any investment decision.

The value of your investment may go down as well as up. Past performance is not a reliable guide to future returns. You may get back less than you invest.

.jpg")

into employment. </p>")