Dairy price slump drags down average 2015 family farm income

The weakness of the euro; low oil prices; growth in the UK, US and Irish economies; and inflation in China, all had their effects on Irish farm incomes in 2015.

And they will continue to do so in 2016.

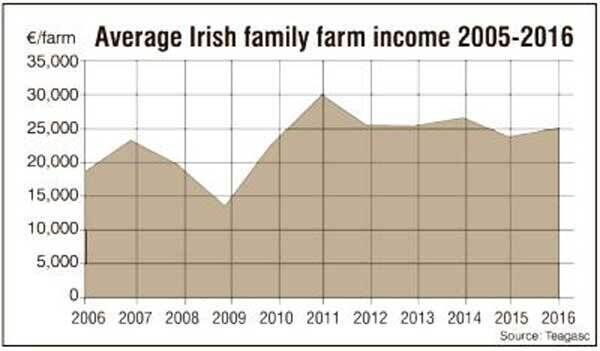

On average, family farm income is estimated to have fallen by 9% to an average of €24,008 in 2015, according to the economic review and outlook of Irish agriculture published by Teagasc.

But a 5% incomes recovery is expected in 2016.

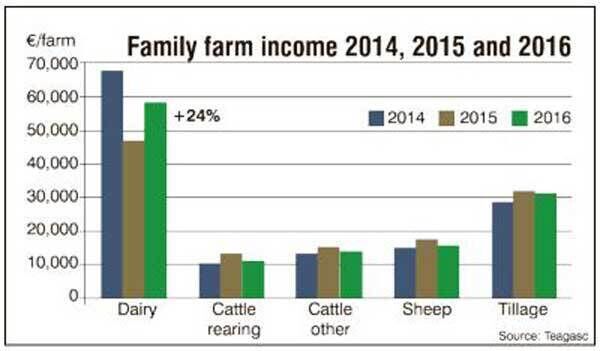

The Teagasc report illustrates how heavily the health of Irish farming depends on the dairy industry.

Profit margins in the cattle, sheep and cereal enterprises all increased in 2015, but not by enough to compensate for a 26% decline in margins in dairying.

In 2016, recovering dairy profitability is expected to lift the averages, but cattle farming profit margins are expected to decline.

And of course Teagasc experts couldn’t say if the kind weather conditions which helped Irish farmers in 2015 will return in 2016.

Euro weakness

The euro has been worth less than 75 pence sterling for most of 2015.

In the years from 2009 to 2011, it was exchanged for between 85 and 90 pence.

Likewise, its exchange rate with the dollar during 2015 was close to €1.10, compared with €1.30 to €1.40 for most of the period since 2009.

The weak euro has been good for the tourist industry, as Americans and British find visiting here is cheaper.

The weak euro has also helped the competitiveness of food and agricultural exports.

However, necessary imports such as soya and maize, sourced in the dollar area, are dearer.

Oil prices

The other major external development in 2015 has been the crash in crude oil prices, which has been somewhat reflected in the price of oil and diesel at the pumps, and has reduced the cost of farm inputs.

The fall however was not as great as the statistics might suggest, as oil prices are designated in dollars, and the fall in the euro smoothed the decline in oil prices.

Other external factors which affected the sector in 2015 were the Russian embargo on food imports from the EU, which particularly affects the dairy sector, and contributed to lower milk prices and significant increases in Chinese domestic pork prices (which may lead to increased imports in order to limit inflation).

Cattle

The big story for Irish cattle farmers in 2015 was the increase in prices obtained, while costs of production remained stable. This led to improved profit margins.

But Irish cow numbers are 5% higher in 2015.

The increase in beef supply from the growing herd is greater than the increase in demand for beef; therefore the market for beef is expected to be weaker in 2016, which will reduce profit margins.

The same big trend follows for the EU as a whole, due to increasing total cow numbers.

Sheep

Demand within the EU for lamb is growing at a faster rate than supply (and imports from Australia and New Zealand are stable).

This has led to a modest improvement in prices in 2015.

As the UK is one of the principal markets for Irish lamb, the movement in the euro-sterling rate has also had a favourable effect on prices for sheep in Ireland, from the farmers’ point of view.

With stable production costs completing the picture, profit margins per hectare improved in 2015.

This trend is expected to continue into 2016, with a further 3% increase in prices predicted by Teagasc, and further increases in profit margins as a result.

Cereals

Worldwide, there has been a record harvest of cereals in 2015. There are “comfortable” levels of grain in stock.

There is no reason why prices should rise in the short term, but some increase is projected before harvest time in 2016.

In Ireland also, there have been record yields, for the past three harvests.

The likelihood therefore is that yields in 2016 will return to normal levels.

Costs are not expected to change. Not much change in profit margins is therefore expected.

Pigs

There are fewer than 300 commercial pig enterprises in Ireland, but the average size is the largest in Europe, at 540 sows.

The average pig unit is responsible for €1.7m of exports annually.

The main feed inputs are wheat, maize and soya beans.

Worldwide production of each of these has been increasing rapidly in recent years, leading to a reduction in feed costs on Irish pig farms in recent years.

The volume of production reached a record level of 3.65 million pigs slaughtered in 2015, but this is only about 3% of EU production (the major players are Germany with 43m million slaughtered in 2015, and Spain with 30m).

The profit margin over feed is measured in cents per kg of pork.

The estimated level in 2015 is 37 cents, which is significantly lower than the five-year average (42 cents), or the 20 year average (48 cents).

Prices for the major feed ingredients are expected to increase in the short term (by 3% in 2016).

But Teagasc experts note the unknown factor in relation to feed prices, the impact of the El Nino weather pattern, which stems from warm ocean water in the central and east-central equatorial Pacific.

The current El Nino is the third most powerful recorded, and it could have major implications for soya bean yields in South America, and therefore for compound feed prices on Irish farms.

Prices for pork are expected to increase by about 6% in 2016, leading to some recovery in profit margins.

Eamonnpitts@gmail.com