New home buyers: What is the best mortgage for me?

A lifetime decision: When choosing which type of mortgage is best suited to you, always take professional advice.

The common-or-garden variety of mortgage and the one that the vast majority have is the Annuity Mortgage.

It’s the standard type which involves the lender (bank or mortgage company) advancing a large sum of money to the borrower, allowing them to pay the purchase their home.

The borrower commits to making a series of monthly repayments over an agreed time period (the “term” of the mortgage). Typically, the term is between 25 and 30 years.

The monthly repayments are a mixture of the interest and the principal (the original sum borrowed). Over the term of the mortgage, the repayments are evened out to be the same amount every month.

At the beginning of a mortgage term, for example, the majority of what you’re paying is composed of interest, with only a very small percentage of your monthly payment going to pay off the principal. As the years roll on, however, those percentages are gradually reversed.

The percentage of monthly repayment going towards the principal increases as that going to interest decreases, so that the principal reduces at an exponential rate.

The isn’t the only type of mortgage available and a very small percentage of people choose other options.

The involves a mortgage where your regular repayments against the principal are made alongside regular payments into an endowment fund. When the term is over, the principal is paid off fully and the amount accumulated in the endowment fund should be enough to pay the interest bill with some cash to spare.

Then there’s the As the name suggests, the idea is to establish a pension fund while you pay off the principal on your mortgage. When that is done, the timing might even coincide with pension time but in any case, the pension fund pays out when it is time to retire.

There is one other type of mortgage that works along similar ‘side-by-side’ lines – namely the which is also referred to as the

Central Bank rules have undergone an important change recently and since the 1st of January 2023, borrowers can borrow up to four times their gross income (previously, the limit set was 3.5 times your income). This limit applies to first-time buyers only. For example, if you earn €50,000 before tax, then you will be allowed to borrow no more than €200,000 (4 x €50,000).

There are still certain exceptions to this rule. More leeway can be given by lenders to those who are defined as being in the “high-earning” category of breadwinners; which is, as things currently stand, someone who earns more than €50,000 gross per annum. As a couple applying together for a mortgage, the “high-earning” definition comes in at a combined income of €70,000. Another exception can be instigated by the bank itself. They have the discretion to break the income rule for a limited number of cases per year, with most of these exceptions being used up in the earlier part of the year.

All of that discretionary power with lenders will often depend on how good a candidate for a loan that is presented before them. If you have a good savings record and/or a good track record as a borrower, that would obviously stand to you, as would certain professions that would be regarded as stable and with a positive future.

Here again, Central Bank rules apply and the Loan-to-Value (LTV) ratio they have set is 90%. Therefore, no bank or lending institution will be allowed give someone a loan for any more than 90% of the price of the house or apartment.

So, you need to have a deposit of at least 10% of the price of your home. If you happen to have more than this, then you’re very likely to get a more competitive interest rate from your lending institution.

The Help-to-Buy (HTB) scheme has been in place for a number of years to help the first-time buyer sector. It means that borrowers can effectively reduce the minimum deposit figure. It’s a very big help in the current climate with rents continuing to climb sky high, making it increasingly difficult for potential home buyers to save for their deposits.

Under the HTB scheme, a first-time buyer who wants to buy a new home is entitled to a tax rebate of up to 10% of the purchase price up to a maximum amount of €30,000. You’ll find that the majority of lenders will facilitate this procedure but it would be wise to double-check in discussions with them.

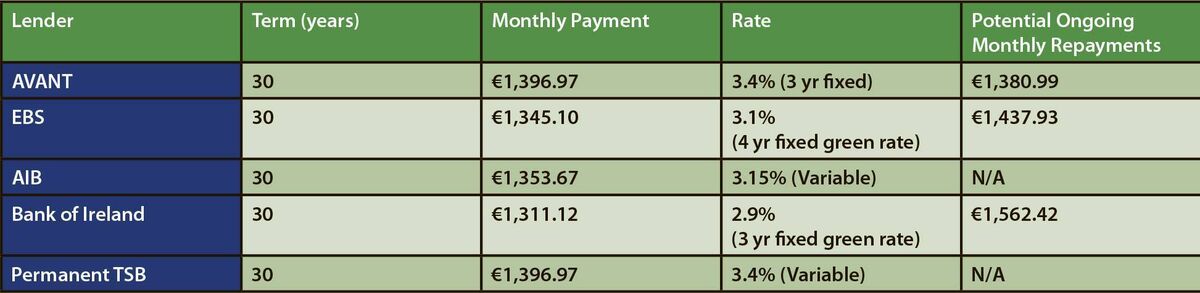

In the table below, you can see some up-to-date examples of rates and monthly repayments from some of the top lending institutions in the country. The examples are based on a first-time buyer buying a home for €350,000 with a 10% deposit of €35,000 (i.e. a mortgage of €315,000). The rates given are standard for first-time buyers and don’t take account of potentially better rates that can be got by, for example, opening a current account with the lender and/or having a higher deposit. In addition, some banks offer ‘cash back’ on the loan. Also, many rates are “green”, corresponding to a high BER (Building Energy Rating), which all new homes normally have.

When choosing the best rate, it is best to look at it simply. Every bank has a different twist to get you in their door – from cashback offers to green encouragement. Nowadays, we are also at an interesting juncture where the fixed and variable rates are quite similar. The simple truth, however, is that the best rate is the lowest one because it involves you parting with the least amount of money going out of your pocket every month.

After that, it’s a matter of attitude – whether you prefer to run with a variable rate or fix the rate for a certain period of time. The attraction with the fixed rate is that you don’t need to worry about the rate changing during the fixed period. The variable rate might get you better value but it’s liable to change with barely two months’ notice.

Right now, rates are rising after an unprecedented long period of low stable rates. Judging by the good value still being offered in fixed rates, however, it doesn’t look like rates are going to go much higher over the next few years, but there’s no crystal ball available.

You need to ensure to make provision for the following costs involved in getting a mortgage:

For many people, the first time the require the services of a solicitor is when they buy a home for the first time. And it’s unlikely to the be the last time you’ll require legal counsel. The main element to keep in mind when choosing a solicitor is trust. There’s a lot at stake when buying a home and there are usually one or two complexities/frustrations along the way so having someone you know you can trust and work with is of great importance. An approximation for this cost would be around €2,000.

This used to be a very big bill but nowadays the Government takes 1% of the price of your property from you for the privilege of buying your own home, unless your home costs more than €1 million. If that’s the case, you pay 2% on the amount over the million.

There is no avoiding this one – and with good reason for all concerned. The basic legal requirement is that the life policy will pay out the outstanding mortgage balance in the event of the demise of one of the spouses. From here, you can enhance the product to cover ancillary risks, such as Serious Illness Protection or Income Protection. Shopping around is advised as rates can vary greatly, but around €250 per year should see you right for the basic package.

Another vital one that you should shop around for and you should pay approximately €400 per year.

It’s a necessary evil that you also must cough up for as the lender won’t release the loan cheque until after an independent valuation of your home is carried out. Expect to pay approximately €200.

There isn’t any legal obligation to have a surveyor carry out a structural assessment of your new home but your solicitor will always advise it, it’s normal practice in Ireland to do so, and it’s probably a good idea, at a cost of approximately €300.

CONNECT WITH US TODAY

Be the first to know the latest news and updates