New Homes: Essential advice on mortgages and finance

As a borrower, when you get your first year’s statement from the lending company, you might notice that the principal hasn’t reduced much. Don't worry, as you get towards the end of the mortgage term, the principal amount starts to reduce exponentially.

The number of mortgage types out there are many but there are very few people who choose anything but the normal, common-or-garden variety of mortgage, which is the Annuity Mortgage.

This is the one that the vast majority of borrowers choose each year and it involves the lending institution or bank advancing a sum of money to the borrower to allow them to buy their own home. The borrower(s) then makes a series of repayments once a month over the term of the mortgage (normally between 25 and 30 years) until the principal (the sum borrowed) and the interest (according to the agreed rate or rates) is fully repaid.

Amongst the other mortgage types are the Endowment Mortgage, the Pension Mortgage and the Current Account (or Offset) Mortgage. These three work in a similar way, with repayments on the principal and the interest being made separately from one another.

With the Endowment Mortgage, your regular payments on the principal are made alongside regular payments into an endowment fund. At the end of the term, the principal will be fully paid. Meanwhile, the endowment fund being built separately should be enough to pay off the accumulating interest bill, with some spare cash for the borrower’s pocket.

In the case of the Pension Mortgage, you’re doing essentially the same thing, except that you’re establishing a pension fund instead of an endowment fund; which has different characteristics in terms of potential taxation implications. The idea is to have the mortgage principal paid at about the same time as pension age kicks in for the borrower. The Current Account Mortgage operates the same way, with a fund building up that should pay the interest bill when the principal is paid off.

Each monthly repayment is a mixture of principal and interest and they are levelled out to enable the borrower to make payments that stay the same amount, as long as the interest rate doesn’t change. Towards the beginning of the term of a mortgage, therefore, the vast majority of the monthly payment is going towards the interest.

As a borrower, when you get your first year’s statement from the lending company, you might notice that the principal hasn’t reduced much. But as the mortgage term advances, the ‘interest’ percentage of the monthly repayment amount reduces. Therefore, as you get towards the end of the mortgage term, the principal amount starts to reduce exponentially.

Current Central Bank rules allow people to borrow up to four times their gross annual income. This has been increased from 3.5 times one’s annual income since the 1st of January 2023.

There are many commentators saying that it should be increased again to reflect rising house prices, but the Central Bank also has a duty to ensure that whatever they do doesn’t contribute to house price inflation – hence their reticence to allow people to borrow even more money.

This limit is for First Time Buyers only, in any case. So if you earn €50,000 a year before tax, then you can borrow no more than €200,000 under the normal Central Bank Rules.

There are ways in which you may be able to exceed that amount, however. If you’re defined as being in the “high-earning” category (over €50,000/annum for a single person or over €70,000 for a couple), then you can borrow more than four times your income. The lender itself also has the leeway to break the four-times-income rule for a limited number of applicants every year.

In order to avail of that discretionary lender’s power, you stand a greater chance of success if you can illustrate that you have a good savings record. Or indeed, your record as a borrower from previous loans for cars or other items.

All of these things stand to the potential home loan borrower, as well as certain professions; a stable and high-paying job will be seen as a strong asset by the lending institution and may influence their lending decision towards you.

The answer is 10% of the purchase price. The Central Bank set the rules in this regard and they have set a maximum Loan-to-Value (LTV) ratio of 90% of the purchase price. If you have managed to save a deposit of more than 10% of the purchase price of the property you’re going to buy, then you’ll get a better rate from the lender.

For most people, however, it’s an achievement to manage to get the minimum 10% deposit. While that figure isn’t negotiable per se, what has changed in recent years is that Government schemes have given First Time Buyers an advantage in the process.

With the HTB (Help-to-Buy) scheme, you can effectively reduce the minimum deposit figure. Under the HTB, a First Time Buyer purchasing a new home is entitled to a tax rebate of up to 10% of the purchase price, up to a maximum of €30,000.

Furthermore, the First Home Scheme is a shared equity scheme which also significantly reduces the amount that a borrower needs to put forward as a deposit. Using the two schemes in combination (depending on the circumstances) can sometimes mean that in effect, a borrower might only be looking for 70% of the purchase price, having saved a 10% deposit.

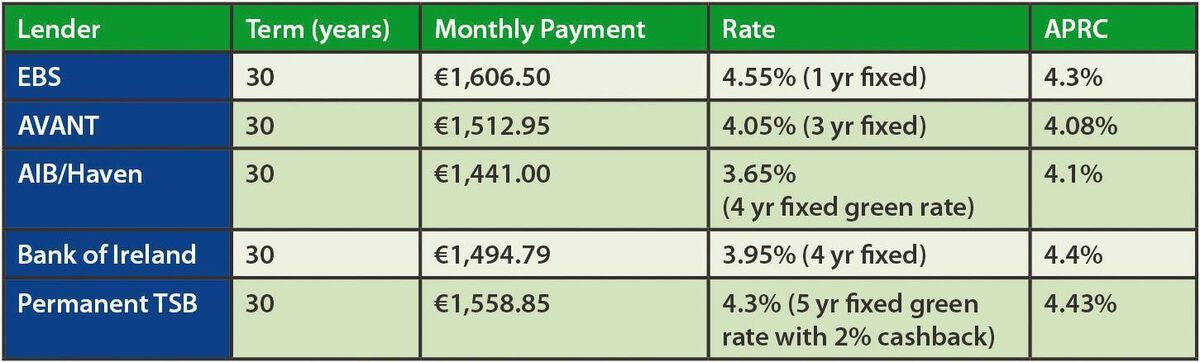

The table below offers some current examples from some of the top lending institutions in the country of rates and the corresponding monthly repayments. The examples are based on a First Time Buyer purchasing a house for €350,000 with a 10% deposit (i.e. a mortgage of €315,000). Some banks will offer better rates if the BER figure is good (greener mortgages) and/or if the borrower opens a current account with the lender. Some banks also offer ‘cash-back’ incentives.

Every lender has its selling points. Some will offer you cash back in your hand and many of them (including some of the examples above) will offer you better rates if your new home is more carbon-neutral; the so-called Green Mortgage.

Some of them will be better to deal with than others, which is another aspect to consider again, for the times to come when there may be some bumps along the road.

There isn’t a whole lot in the difference of rates that lenders are offering. All in all, it pays these days to fix the rate for as long as possible. Even though there have been interest rate increases over the last two years, we’re still living in an era of low interest rates (in the early 1990s, there were mortgage interest rates of around 14%) and all the indications are that the rates are due to get lower in the coming year.

A long time ago, one person I knew working in one of the biggest lenders in the country advised me that the best rate is always the lowest one. All things considered, there might be something in that. I would say that you owe it to yourself to keep the rate as low as possible and you want to deal with people that you can get on with.

When getting a mortgage, there are always additional costs that need to be paid. Each one isn’t a huge cost in itself, but together, they add up to a significant sum that you need to set aside:

This should be one of the first ones you think of, but it comes as a surprise to some that you absolutely have to ensure that your home is insured. It can vary from one company to another and from one year to another, but you should be paying around €400 annually.

It’s a basic legal requirement that in the case of the demise of the borrower or one of the borrowers, a life assurance policy is in place that will pay out the remaining balance of the mortgage. One can add to this, of course, in having a sum larger than the balance sum pay out. You can also get serious illness cover or income protection too, but the basic package should be around €250 per year.

For first-time buyers, this is often also the first time that they are engaging the services of a solicitor. Trust is the most important element to consider, with cost being the secondary element. Somewhere in the region of €2,000 would be a normal fee to expect.

Any solicitor will advise you to have a structural assessment carried out on your new home, even though it isn’t a legal requirement. With strong building regulations nowadays, many buyers don’t see the need. If you do continue with this normal practice in a home purchase, however, expect a fee of around €300.

The lender won’t release the required loan cheque until an independent valuation of the home you’re buying is carried out, at a cost to you of around €200.

Nowadays, this bill represents 1% of the purchase price of your property, unless your home costs over €1 million, in which case you pay 2% on the amount exceeding the million.

CONNECT WITH US TODAY

Be the first to know the latest news and updates