3,800 repossession orders granted as home seizures to rise

Despite this, the CEO of the Irish Mortgage Holders Organisation has warned the rate at which such orders are issued will increase as the influence of vulture funds is felt in the Irish market.

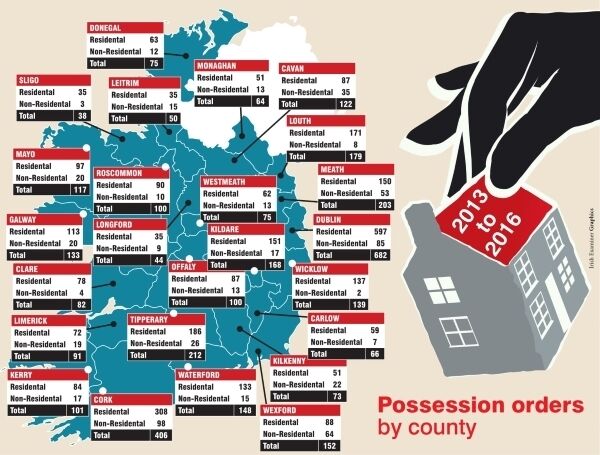

An analysis of the figures released by the Courts Service show almost 84% of the orders granted from 2013 until 2016 relate to residential properties.

Repossession orders can be granted in cases such as contested wills. However, while a breakdown of the applicants in the cases was not available, the Courts Service said the vast majority of cases were instances where banks sought to move on customers in arrears.

A total of 3,779 repossession orders were issued over the 2013-2016 period, 3,163 of which related to residential properties.

While just 343 orders were issued in 2013, the following year saw a drastic increase with 1,063 orders granted, followed by 1,285 in 2015 — the highest number recorded over the period. In 2016 1,088 orders were issued.

Unsurprisingly, Dublin recorded the highest number of repossession orders over the four years, with 682 granted. Cork (406), Tipperary (212), Meath (203), and Louth (179) rounded off the top five. The lowest number of orders issued between 2013 and 2016 was in Sligo (38), followed by Longford (44), Leitrim (50), Monaghan (64), and Carlow (66).

The Courts Service categorised repossession orders as either “residential” or “non-residential” until September 2014, when it split the residential category into primary home or buy to let.

This breakdown shows that the majority of repossession orders are for primary homes. In 2016, for example, 854 of the 1,088 repossession orders issued were on primary homes, 62 were buy to let, and 172 were categorised as “other/unknown”.

In 2015 — the year with most orders issued over the period in question — 919 related to primary homes, 148 were buy-to-let properties, and 218 were other/unknown.

Examples of “other/unknown” properties include land sites and commercial properties.

Despite this, David Hall, CEO of the Irish Mortgage Holders Organisation, has warned that he believes the rate of orders will only increase in the coming years.

“Repossessions are low due to the courts’ reluctance, and multiple changes to various restructuring arrangements including the introduction of the insolvency service,” said Mr Hall.

“There is a tsunami coming as many banks are waiting to outsource the repossessions by selling to vulture funds. Bank and vulture lovers will be judged by history as having been wrong. Thousands can’t pay and will lose their homes unless a radical approach is taken.”

A recent report by the Central Bank warned that, left to the own devices, Irish banks will do little to tackle the mortgage arrears crisis.

According to Central Bank figures, the overall value of all arrears on all mortgages in distress stood at over €2.51bn at the end of 2017. It said 14,000 households are at risk of losing their property. It revealed 28,946 primary dwelling house loans were in arrears of over two years as of last December — and these account for 60% of all mortgage cases in arrears for more than 90 days.

“Over half of the cases progressing to long-term arrears are classified as involving the potential for loss of ownership outcomes,” the article warned.

It said those losses would either be through voluntary actions, whereby the borrower gives the property back to the bank or sells it as part of settling their debts, or through enforcement, where a repossession order is granted by the courts.

There has been a total of 8,195 cases involving primary dwellings that resulted in loss of ownership since July 2009, with 2,722 resulting in repossession from a court order and 5,473 properties surrendered voluntarily.

Thousands of home repossessions approved by courts in four years

‘Worst yet to come’ say campaigners as vulture funds expected to step up moves against people in arrears, writes

Thousands of repossession orders have been granted by courts in just four years — but that maybe just the tip of the iceberg.

Figures released to the Irish Examiner show a total of 3,779 repossession orders were issued over the 2013 to 2016 period, 3,163 of which related to residential properties.

In 2013, 343 orders were issued, the following year saw a drastic increase with 1,063 orders granted, followed by 1,285 in 2015. The highest number recorded over the period. In 2016, 1,088 orders were issued.

Over the four years, 682 of the orders were issued in Dublin, and 406 in Cork. Tipperary (212), Meath (203), and Louth (179) followed in terms of the counties with the highest orders.

Both the Central Bank and the Irish Mortgage Holders Organisation (IMHO) have warned that thousands of homes are at risk of repossession in the coming years, with the latter placing the blame firmly at the door of vulture funds.

In April, a Central Bank report on the issue of on resolving non-performing loans (NPL), warned that 14,000 households in Ireland are at risk of losing their property.

It said that 28,946 primary dwelling house (PDH) loans were in arrears of over two year as of last December — and that these account for 60% of all mortgage arrears cases in arrears more than ninety days.

The report stated there has been a total of 8,195 cases involving primary dwellings which resulted in loss of ownership since July 2009, with 2,722 resulting in repossession from a court order and 5,473 properties surrendered voluntarily.

The figures released by the Court Service to the Irish Examiner show 3,163 residential properties — which consists of both primary dwellings, second homes, and buy-to-let properties — were subject to possession orders over the 2013-2016 period.

The IMHO believes the worst has yet to come, and that banks are more reluctant to pursue possession orders than the vulture funds who have come in to buy up loans from Irish institutions.

The organisation has accused Ulster Bank of ‘not caring’ about its customers following the announcement that it is to seek the sale of mortgages currently on its books.

“The banking system crashed the country and the state decided banks were more important than citizens and propped them up by pumping billions into some banks thus supporting the entire sector,” said IMHO CEO David Hall.

“Now banks, having tortured those in mortgage arrears for years, they are outsourcing their dirty work to vulture funds and treating citizens in trouble with contempt.

“Instead of getting vulture funds to do their dirty work Ulster Bank could have engaged in seeking solutions. They could have looked at radical restructuring like debt for equity or providing people an interest for life in their properties.

“They could have engaged with government and local authorities to see how many properties could be transferred to their ownership.

“They could have sought loan purchasers who are interested in something other than the asset.

“Minister for Housing Eoghan Murphy is under pressure trying to grapple with the homelessness crisis that currently exists but the tsunami of repossessions that’s ahead will dwarf the current crisis.”

The scale of the mortgage arrears problem was highlighted by a Central Bank paper.

According to the Central Bank figures, the overall value of all arrears on all mortgages in distress stood at over €2.51bn at the end of 2017, while the outstanding mortgages on those accounts stood at almost €12.82bn.

The Central Bank said people in long-term arrears who had engaged with the bank were “significantly more likely to receive a short-term restructure arrangement than those currently in earlier stages of arrears”.

It warns about taking policy decisions “outside of the scope of” regulators because it may complicate reaching deals with existing borrowers in arrears, as well as “undermine payment discipline, and may lead to lower supply of mortgage credit or higher interest rates for the overall market in the future”.

Reviewing the progress in dealing with NPLs, it says its policies are driven by “putting the fair treatment of those in financial distress at the centre of the Central Bank’s response to the crisis”.

CONNECT WITH US TODAY

Be the first to know the latest news and updates