Pensions — don't know where to start?

Seek expert advice: Let’s say you want to retire at state pension age 66 and draw an annual pension of €50,000. The state pension is currently €13,800 leaving €36,200 to make up. Picture: iStock

“The key is to start!” says Bernard Mulkerrins, Head of Propositions at Acorn Life.

There’s a lot here to take in and pension planning can appear complicated. But, if there’s one take-away message, it’s to get yourself investing in a pension as early as you can, regularly setting aside as much as possible. The earlier you get going, the less it will cost you to set yourself up with a decent income when you retire to maintain the lifestyle you’re used to.

“The best time to plant a tree is 20 years ago. The second-best time is now.” You might say “What’s the rush. Retirement is a long way off and sure I’ll enjoy my life today”. Just be aware of how much that could cost you. The longer your money is invested the harder it will work for you and the less you’ll need to invest overall. Let’s say you want to retire at state pension age 66 and draw an annual pension of €50,000. The state pension is currently €13,800 leaving €36,200 to make up.

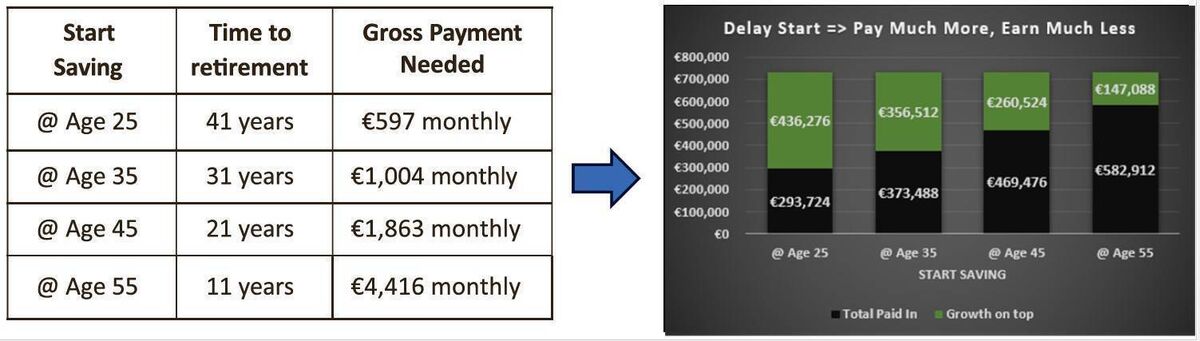

Based on typical annuity rates for a single person, you’ll need €730,000 to fund for this amount on your 66th birthday. Sounds a lot but, if you start early, it doesn’t take as much as you think to get there.

Let’s assume your pension makes 4% annual growth after charges:

Clearly, to retire with this income at 66, each year you wait to start saving makes a massive difference.

Also, it’s common for employers to cover half of the above savings. And don’t forget you’ll get tax relief on what you put in. High rate taxpayers can potentially re-claim 40% of their personal investment (subject to age and salary-related limits).

Let’s break down the example of starting at age 35 to get €730,000 at 66:

The figures in the graph are calculated assuming that the monthly payments remain fixed and do not increase. The cost of buying the pension is based on market annuity rates obtained by Acorn Life to purchase a level annual income payable for life for a person aged 66 at retirement.

Increases in the cost of living can erode your wealth. Inflation has the opposite compounding effect to the investment growth shown in the table above. Irish inflation has averaged 7.5% over the last two years. Put simply, this means what cost you €100 two years ago will cost you €116 today (CPI to August 2023). Consider that compounded over 30 years! The growth you achieve on your pension pot will help you maintain the purchasing power of your savings.

Pensions are a long-term investment and ideally your investment needs to produce returns greater than inflation to maintain the purchasing power of your retirement income. To achieve this, you must be willing to take on a certain amount of risk while your money is invested. And there will be times when you take a hit on your investment. The key is to have a long-term investment horizon and to ride out periods of volatility.

While past performance should not be considered a guide to future performance, stocks, measured by the S&P500, have achieved 6.7% yearly growth (inflation-adjusted) in the 50 years to end August (Source: ). A pension through its long-term nature is the perfect vehicle to take advantage of stock market performance.

A good financial advisor will help you manage your risk profile as you progress through life and help select funds suitable for your needs. For example, you might select funds with higher risk exposure early on to target real growth, maybe moving to funds with more stable returns as you approach retirement.

Irish people often favour tangible investments such as land or bricks and mortar. But investment through a pension has one critical advantage over all others. The government is incentivising retirement saving through tax relief. No other investment will give you such a guaranteed one-off return on each personal contribution (tax relief is 40% for high rate taxpayers and 20% for standard rate taxpayers).

On top of this your money, and growth on your money (just as important), grows tax free while gains on non-pension investments are subject to regular taxation. Such tax drains the growth potential of an investment. With a pension, tax doesn’t kick in until you eventually draw down your money in retirement. But, even then, part of your pension can be taken tax-free. There’s a significant tax-free lump sum allowed and, after that, what you draw down is taxed as income. Your financial advisor can help you manage your drawdown to limit what you pay at the high rate.

And don’t forget that a good pension will offer you a broad range of investment options. You can pick a fund that invests in assets aligned to your preferences whether that be company shares, property, fixed interest or pretty much anything else tradeable on a recognised exchange.

What type of pension solution?

If you’re a member of your employer’s pension scheme, keep it going! You will achieve all the relevant tax reliefs and your employer is probably contributing to it. Just make sure it’s on target to achieve your goals.

You have options if you’re not an active member of a company pension scheme, whether you’re an employer, employee or self-employed. One of the most popular and simplest solutions is a Personal Retirement Savings Account, PRSA. There are several advantages to a PRSA, which your financial advisor can explain in detail. These include:

- Regulatory rules on charges … meaning good value for money.

- Flexibility on when you pay in … you can pay regularly, take breaks or pay in lump sums.

- Pension contributions are extremely tax-efficient … in addition to your own, if applicable, your employer can make separate unlimited contributions free of corporation tax at any time. Just watch the lifetime “standard fund threshold” of €2m which your advisor can explain.

- Retirement draw-down is extremely tax-efficient … 25% can be taken tax-free immediately with the rest subject to income tax.

- Portability … take the PRSA with you if you change jobs and your new employer can also contribute.

It’s easy with the right support. Find a financial advisor who you know and trust and who will take you through a full financial review to help you figure out what you can afford to save regularly for your retirement.

Your financial advisor will recommend the best pension solution for you and help you to get started. Affordability is important. Once money is in the pension, it cannot be accessed until you retire. A good advisor will meet you regularly to monitor the performance of your chosen investments and help you make adjustments from time to time to keep you on track for your retirement goal.

Most people in Ireland make little or no provision for retirement. Sadly, this means they are faced with living on the state pension. When you put a little away regularly, a pension will do the heavy lifting to help you maintain the lifestyle that you are used to in retirement. Your tax return deadline is just around the corner (October 31st, or November 15th if you submit through ROS) … don’t delay!

CONNECT WITH US TODAY

Be the first to know the latest news and updates