You can retire well on 50% of your gross income

Having a significant nest egg allows you the flexibility to choose the type of retirement you want.

When it comes to planning for retirement, people take different approaches: Some do nothing at all, leaving their fate to chance. Others pay diligent attention, planning young, while saving early and often. The rest lurk somewhere in between.

For all of their differences, the bearers of every one of these approaches have at least one thing in common: All would benefit, or at least be reassured, by having a financial health-check with a retirement savings expert.

On the choices people have for funding any financial shortfall that might arise when retirement comes, Ian Kennedy, co-founder of the Pensions Support Line says: “There are many options, such as rental income from an investment property, or savings in a bank or post office.

“Most aim to meet this shortfall by contributing to a pension throughout their working life because of the generous tax reliefs available. The earlier you can start paying into a pension the better. Even if it means you can only save a small amount each month. That’s because the longer you leave it, the more expensive it gets.”

Ian Kennedy advises that we should aim for a retirement income of approximately 50% of your gross pre-retirement income. This is a good rule of thumb of the income to aim for in retirement.

Kennedy says: “If you earn €47,000 per annum on the day you retire, €23,500 would be an appropriate number to aim for. Now, if you were to receive a full State pension of €12,900 per annum [figure correct pre Budget 23 announcement] that would leave a shortfall of €10,600 per annum.

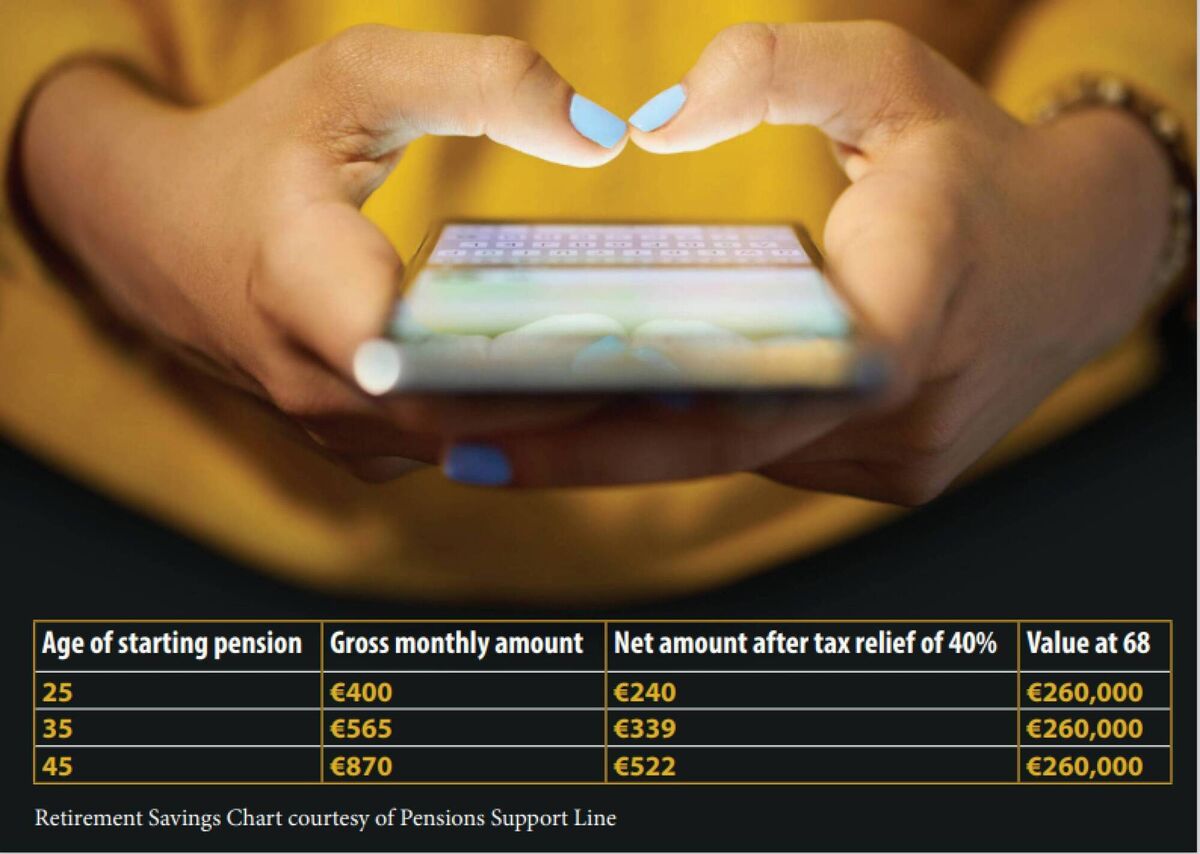

For someone aiming to build up a pension fund of around €260,000, which would give a pension of around €10,600 per annum, Kennedy gives clear advice. He says that the accompanying graphic shows what a person would need to save each month to reach their retirement savings goal, at 68 years of age.

While the cost-of-living crisis is doing us no favours day-to-day, it’s also banjaxing the saving plans of many. According to a Pension Awareness Week survey conducted by Behaviour & Attitudes (B&A) and published in September of this year, it is the given reason why those in Ireland who are without a pension, have either delayed starting one, or postponed their chosen retirement date.

Anyone considering postponing should perhaps skip ahead to the next paragraph now. Not everyone will want to know that early retirement may be a risk factor for mortality. That was the sobering finding from a study published in the Journal of Epidemiology and Community Health. It found that working just one additional year beyond retirement age, reduced the risk of dying (over the 18-year study period) by between 9 and 11 per cent, regardless of health.

That we really need to talk about pensions was clear from the findings of the B&A study, in which almost two-thirds of 25-49-year-olds polled admitted they found the topic of pensions ‘too complicated to understand.’ Among 35-49-year-olds polled, the prospect of saving for retirement was dim, with 72 per cent reporting being financially wiped after essential bills were met.

Hope did not feature highly in the study, in which a substantial 38 per cent of those polled claimed to ‘already know’ they won’t have enough savings when retirement comes around.

This figure was echoed in research published by the Competition and Consumer Protection Commission (CCPC) in recent weeks, where 38 per cent of those polled said they had no pension in place.

The given reasons why were myriad: 20 per cent said they were ‘too young’ with a similar percentage saying they ‘couldn’t afford it.’ 32 per cent indicated they have ‘yet to get around to it.’ Alas, the study also highlights the vast distance that can lie between planning to get around to it and actually doing so: Amongst 55-64-year-olds polled in the CCPC survey, a substantial 23 per cent reported having no pension in place. Some believed the State would deliver, with 77 per cent expecting to qualify for a contributory pension from that source on retirement. Tellingly, only 32 per cent of those questioned, knew how much the State pension is per week.

Retirement means different things to different people. For some, it might involve working methodically or even sporadically through a bucket list. For others, it might mean the dream of pursuing new hobbies, or spending more time doing what you love.

For Fonz Scanlan, financial planner and wealth manager at Money Smart, a ‘good retirement’ does not necessarily entail being young and rich when you retire: “It means you have the ability to step back from work at a time that is right for you, into a life that continues to be enjoyable and meaningful,” he says.

Pointing out then that ‘having a significant nest egg allows you the flexibility to choose the type of retirement you want,’ he continues: “The only way to build that nest egg is to spend less than you earn and invest the difference, all through your working life if possible.

“While income surpluses should go to a pension from a tax efficiency point of view, life is for living and the central aim of good financial planning is all about getting the lifelong saving / spending balance right.

“That's why we should all try to picture how we’re going to spend our retirement years and, long before retirement, plan a lifestyle that we can realistically support financially.” On the topic of how many of us plan to retire on nothing but the State pension, Fonz Scanlan says: “In January of this year, the CSO reported that one third of the working population has no pension coverage outside of the State pension.

Advising that this is very worrying because it is extremely difficult to live solely off the full State pension, he continues: ”And you may not qualify for the full amount. Plus, you could be 67 or 68 years of age by the time you get it, which could be quite a few years after you are willing or able to work.

“While this figure will decrease with auto-enrolment, there remains the problem of those with some form of private pensions and savings not having near enough for a comfortable retirement.

“This is not just because many people simply can't afford to make significant savings. It’s also because many of us underestimate how long we're going to live and how much we'll want to spend in retirement.

“Health and wellbeing often improves through early retirement, not to mention spare time. With all that, comes a desire to see new places and try new things — which means spending more.

“Then later in retirement, when travel spending decreases, there may be ever larger medical and care bills which may not be covered by your health insurance. Ultimately, there’s only one way to prepare for retirement and that is to save.

“Take a small bit of pain now — by reducing spending to create a surplus — so as to avoid a whole lot more pain in retirement."

CONNECT WITH US TODAY

Be the first to know the latest news and updates